- Nerd Out on Business

- Posts

- 15 Years, $0 Revenue, and a $245M Bet on Batteries

15 Years, $0 Revenue, and a $245M Bet on Batteries

Westwater Resources spent $120M building a graphite plant that could revolutionize America's battery supply chain. Too bad they're down to their last $4.5M with construction frozen and debt financing stuck in limbo.

Nick Horob

August 15, 2025

Today I'm digging into Westwater Resources (WWR), and honestly, I never expected to come across a publicly-traded company with 15 years of no revenue.

Some quick back story before you dive into the full report:

• The setup: Former uranium miner that saw the EV wave coming and pivoted to battery materials in 2017 • The twist: They're building America's first graphite processing plant... with just 3 months of cash left • The numbers: $0 revenue since 2009, burning $12M/year, need $150M yesterday • The irony: Already sold 100% of their future production to SK On and Stellantis

Here are a few additional interesting things to highlight:

• They turned Chinese trade tensions into a (potential) business moat (170% tariffs on competitors). • Classic case of being right about the trend but wrong about the timing • They are actively trying to raise $150 million of funding. Yesterday, they annoucned a that they are making progress in their Q2 Business Update.

All-in-all, WWR is walking the plank as we speak. As someone who would like us to have more domestic commodity production, I hope they can find their financing.

With that, I'll see you tomorrow!

Nick

TL;DR

Pre-revenue battery materials company building America's first commercial graphite processing facility in Alabama

Former uranium miner that pivoted in 2017, betting everything on the EV battery supply chain opportunity

Currently burning $12M annually with only $4.5M cash remaining (3-4 months runway)

Despite zero revenue since 2009, pre-sold 100% of future production to major automakers SK On and Stellantis

Stock down 90% from 2021 highs as financing delays threaten survival

Key lesson: Impressive strategic vision (domestic battery supply chain) can't overcome poor execution timing and inadequate capital

The 30,000-Foot View

Westwater Resources operates as a development-stage battery materials company focused on producing battery-grade graphite for electric vehicle anodes. The company has generated zero revenue since ceasing uranium operations in 2009, making it one of the longest pre-revenue pivots in public markets.

Business Model Breakdown:

Primary Product (70%): Coated Spherical Purified Graphite (CSPG) for EV battery anodes

Secondary Products (30%): Natural graphite concentrate and graphite fines for industrial applications

Current Status: Qualification line producing ~1 MT/day for customer testing; commercial production indefinitely delayed pending $150M financing

Key Statistics:

Market Cap: $59M (down from $500M+ peak)

TTM Revenue: $0

Net Income (TTM): -$12.4M

EBITDA (TTM): -$11.7M

Cash Burn Rate: ~$1M/month

Employees: 32 (down from 40+)

Industry Classification: Battery Materials/Critical Minerals

Headquarters: Centennial, Colorado

Primary Operations: Kellyton, Alabama

Company History

Foundation Era (1977-2009)

1977: Founded as Uranium Resources Inc. in southern Texas, riding the nuclear power boom

1977-2009: Operated multiple uranium mines, producing over 2,500 tonnes before operations ceased

2009: Uranium prices collapsed post-Fukushima, forcing production shutdown

Transition Period (2010-2017)

2010-2016: Zombie company phase - maintained listings while burning cash on dormant uranium assets

August 2017: Strategic pivot announced under CEO Christopher Jones, rebranding as Westwater Resources

Battery Materials Era (2018-Present)

April 2018: Acquired Alabama Graphite Corp for ~$10M, gaining the Coosa Graphite Project (41,965 acres) - the largest known graphite deposit in the contiguous United States

2020: Began pilot plant testing, achieving 99.95% purity in lab settings

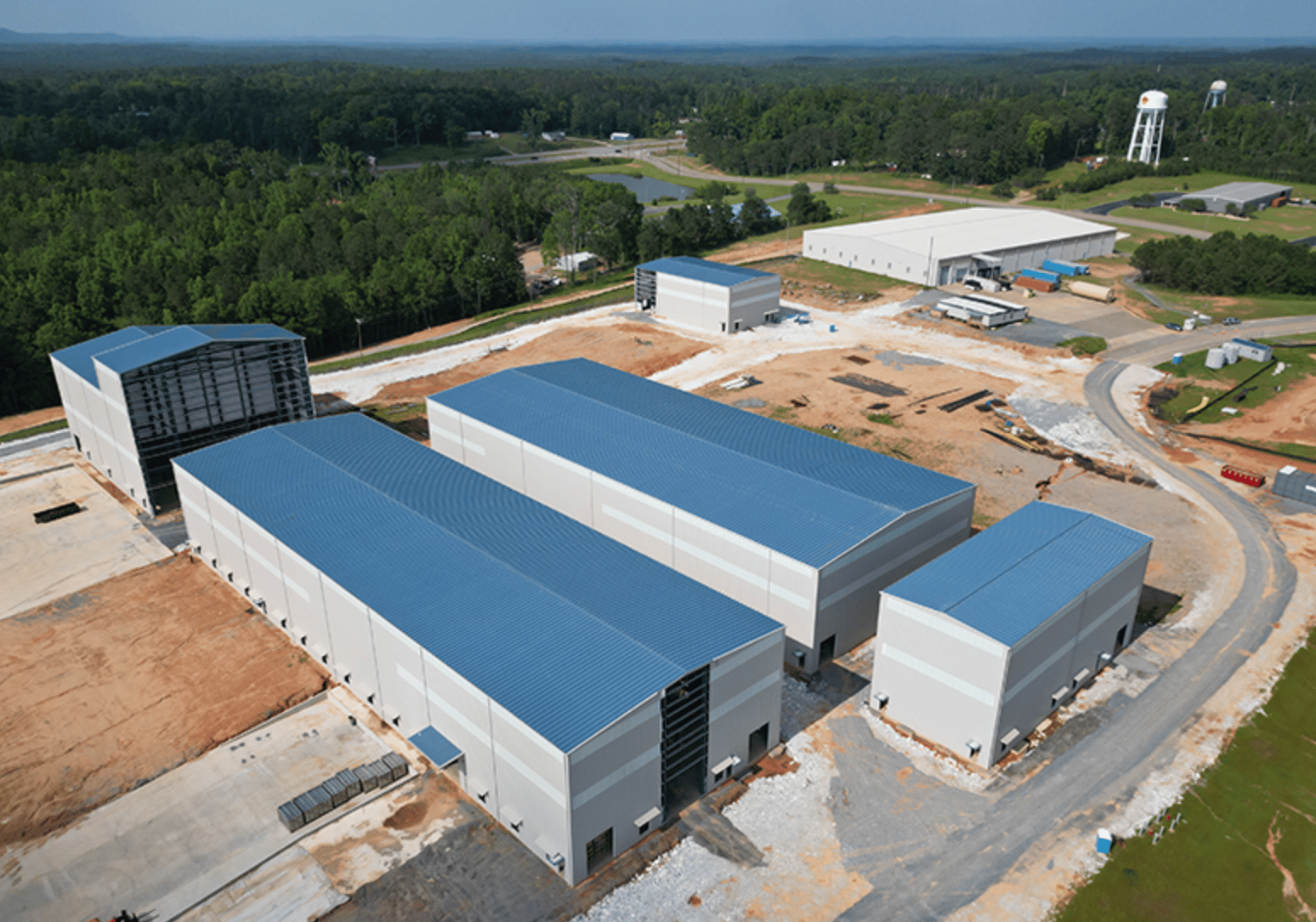

April 2022: Broke ground on $202M Kellyton Graphite Processing Plant with Alabama Governor Kay Ivey

2023: CEO transition from Chad Potter to Frank Bakker amid financing struggles

February 2024: Signed first major offtake agreement with SK On for 34,000 tons over 5 years

December 2024: Commissioned CSPG qualification line but halted construction pending financing

Show Me the Money

Standout Financial Features:

Zero revenue for 15 years straight

Share count increased 14.5% YoY (dilution funding)

Auditor "going concern" warning issued

Financial Data

Metric | FY 2022 | FY 2023 | FY 2024 | TTM |

|---|---|---|---|---|

Revenue | $0 | $0 | $0 | $0 |

Gross Profit | N/A | N/A | -$999K | -$999K |

Gross Margin | N/A | N/A | N/A | N/A |

Ops Profit | -$11.8M | -$13.0M | -$11.2M | -$12.1M |

Ops Margin | N/A | N/A | N/A | N/A |

CapEx | N/A | $58.3M | $4.6M | ~$5M |

Net Debt | -$50M | -$10M | -$3.1M | -$3.1M |

The N.O.O.B. Nine — Competitive Powers

The Nerd Out on Business Nine is made up of Hamliton Helmer's famous "7 Powers" of competitive advantage (Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power) combined with two of my own (Data Flywheel and Distribution Advantage).

Power | Score | Rationale |

|---|---|---|

Branding | 2/5 | ULTRA product line attempts differentiation in commodity market |

Data Flywheel | 1/5 | Minimal data advantages |

Process Power | 3/5 | Patent-pending purification achieves 99.95% purity |

Scale Economies | 2/5 | Phase I capacity of 12,500 MT/year is tiny vs competitors |

Switching Costs | 3/5 | 18-24 month qualification periods create stickiness |

Cornered Resource | 4/5 | Owns largest known graphite deposit in contiguous U.S. |

Network Economies | 1/5 | No network effects in commodity production |

Counter-Positioning | 4/5 | Strong anti-China play with 160-869% tariff protection |

Distribution Advantage | 2/5 | Good Alabama location but no unique advantages |

Average Score: 2.4/5 - Strategic positioning strong but execution capabilities weak.

Memorable Marketing

Westwater's B2B industrial marketing strategy centers on exploiting supply chain insecurity and geopolitical tensions. With zero traditional advertising spend, they've built awareness through strategic PR and political alignment.

Key Campaigns:

SK On Strategic Partnership (2023-2025)

Core Message: "The only domestic solution for IRA compliance"

Channels: Business Wire releases, LinkedIn thought leadership, investor conferences

Hook: Leveraged automaker anxiety about Chinese battery supply dependence

Results: Secured 34,000-ton offtake agreement worth estimated $680M+ over 5 years

Trade War Advocacy Campaign (2024-2025)

Core Message: "Level the playing field against Chinese dumping"

Channels: Congressional testimony, industry coalition building, media interviews

Hook: Positioned company as national security asset

Results: Successfully advocated for 170-869% tariffs on Chinese graphite products

Patent Technology Narrative (2021-2025)

Core Message: "Proprietary purification without toxic chemicals"

Channels: USPTO filings, technical whitepapers, customer presentations

Hook: Environmental superiority over Chinese methods

Results: Patent granted May 2025, enhanced customer confidence

DIY Tactical Takeaways:

Ride political waves: Align your business narrative with current political priorities for free momentum

Convert macro fear into micro sales: Supply chain anxiety post-COVID created urgency they leveraged brilliantly

Join or create industry coalitions: North American Graphite Alliance membership amplified their voice 10x

Choose strategic PR over paid advertising: Zero ad spend yet consistent media coverage

Make customers part of the story: SK On and Stellantis became marketing partners, not just buyers

AI Uses & Opportunities

Current AI Implementation: Minimal to none - company focused on basic survival rather than technological advancement. Potential geological modeling for Coosa deposit optimization, but no confirmed deployments.

Cost-Cutting Opportunities:

Predictive Maintenance: AI-driven monitoring could reduce downtime in 24/7 graphite processing operations by 20-30%

Energy Optimization: Machine learning algorithms to minimize power consumption in energy-intensive purification process (electricity is 15% of operating costs)

Quality Control Automation: Computer vision for detecting graphite flake defects before costly spheronization process

Supply Chain Forecasting: AI demand prediction to optimize $30M+ annual feedstock purchasing from international suppliers

Workforce Optimization: Automated scheduling for 3-shift operations with just 32 employees

Product Value Enhancement:

Battery Performance Prediction: AI models to predict CSPG performance across different battery chemistries and use cases

Custom Material Development: ML-driven formulation optimization for customer-specific requirements (reduce development time 50%)

Rapid Qualification: AI-accelerated testing protocols to compress 18-24 month customer qualification periods to 12 months

Digital Twin Technology: Virtual plant modeling to optimize processes before physical implementation

New Revenue Streams:

Materials-as-a-Service Platform: AI-powered marketplace matching graphite specifications to customer needs

Predictive Pricing Models: Selling graphite market intelligence as subscription service

Carbon Credit Optimization: Automated tracking and monetization of environmental benefits ($5-10M potential)

Technical Consulting: AI-enhanced material selection services for battery manufacturers

Bumps in the Road

Immediate Existential Threats:

Cash Crisis: $4.5M cash vs $12M annual burn rate equals 3-4 months runway maximum

Financing Collapse: $150M debt syndication stalled due to "federal policy uncertainty" and EV credit rollback fears

Going Concern Warning: Auditors explicitly questioning ability to continue operations - the corporate kiss of death

Feedstock Disruption: Primary graphite supplier location affected by regional protests, scrambling for alternatives

Historical Missteps:

Uranium Hangover: Carried dead uranium assets for 8 years post-market collapse, burning precious cash

Pivot Timing Disaster: Entered battery materials at peak hype (2017), started construction at peak capital availability (2022), now facing trough

Leadership Musical Chairs: Three CEOs in three years (Jones 2013-2022, Potter 2022-2023, Bakker 2023-present) creating strategic whiplash

Overpromising Timeline: Originally promised 2023 production start, now indefinitely delayed

Structural Challenges:

Zero Operating Experience: Never operated a commercial graphite facility at any scale

Technology Risk: Proprietary purification process only proven at 1 MT/day pilot scale, not 12,500 MT/year commercial scale

David vs Goliath Dynamic: Competing against Chinese producers with 90% market share and unlimited government backing

Scale Disadvantage: Competitors building facilities 10-15x larger with superior unit economics

Regulatory/Political Risks:

Policy Dependency: Entire business model predicated on continued China tensions and EV subsidies

Permitting Complexity: Graphite processing requires extensive environmental permits in increasingly regulated Alabama

Chinese Retaliation Risk: Success invites potential Chinese export restrictions on necessary feedstock

IRA Rollback Threat: H.R. 1 and changing political winds could eliminate customer incentives overnight

Your Swipe File

Positive Lessons to Steal:

Pre-sell like a pro: They sold 100% of non-existent production by:

Bringing strategic customers (SK On) into product development early

Leveraging macro trends (supply chain reshoring) to create urgency

Offering long-term price certainty in volatile market

Turn regulatory capture into competitive moat: Their tariff advocacy created instant 170% cost advantage:

Joined industry coalitions for lobbying leverage

Framed business as national security imperative

Converted political relationships into protective barriers

Geography as strategy in commodities: Alabama location provides:

Political protection (red state jobs = bipartisan support)

Proximity to Southeast auto manufacturing corridor

Lower operating costs than coastal alternatives

Access to skilled manufacturing workforce

Cautionary Lessons to Avoid:

Pivot timing matters more than pivot vision: They identified the right trend (EV materials) but executed at the worst possible moment:

Started major capex at market peak

Hit financing wall at market trough

Lesson: Keep 2-3 years capital buffer for major pivots

Beware the going concern death spiral: Once auditors flag survival doubts:

Institutional investors flee

Debt becomes impossibly expensive

Suppliers demand cash upfront

Lesson: Always raise capital 12 months early, not 12 weeks late

Don't bet everything on government policy: Their model requires:

Continued China tensions

Maintained EV subsidies

Protective tariffs staying in place

Lesson: Build business models resilient to policy changes